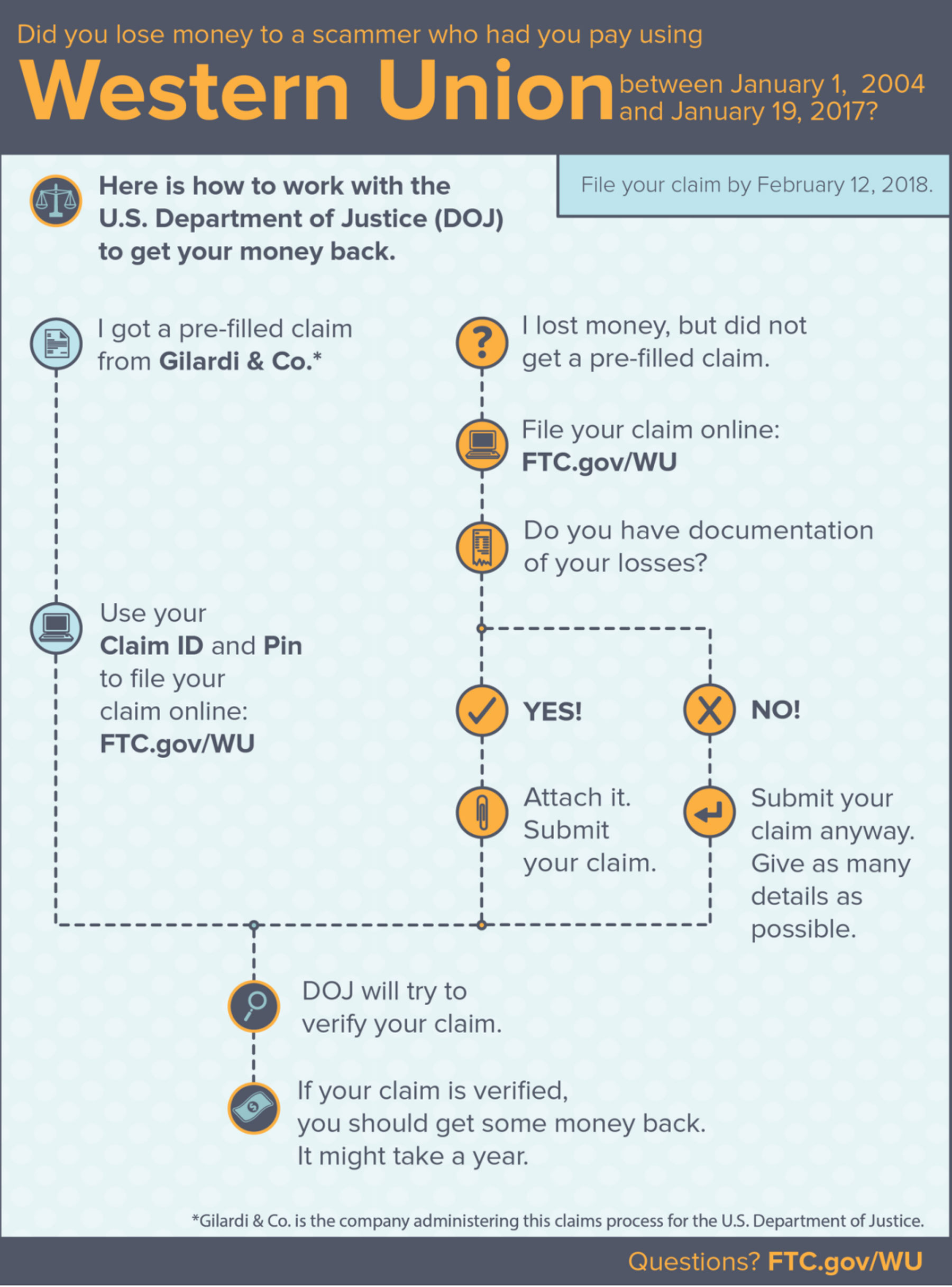

See One which just Are obligated to pay is actually some financial instructions out-of the user Economic Shelter Agency (CFPB). They shows home loan seekers this new strategies they need to get to open up and manage home financing membership. It offers detailed information into rates of interest, and you will demonstrates to you what are similar purchases to the funds, also.

This will make perfect sense. House candidates should know what they are joining. And who would like gotcha minutes otherwise sudden clarifications just after they feels (or actually is) too-late so you can straight back aside?

So, the loan lender legitimately must allow the debtor an official put off closing disclosures at the very least three working days just before closure time.

Increased Disclosure Information: A response to the loan Drama Drop out.

See Before you could Are obligated to pay assists individuals learn the financial techniques, in addition to their selection. New CFPB, a federal institution, works to continue financing strategies fair to have regular people. About agency’s own words: We help in keeping banks or any other economic service providers customers rely on each big date working very.

Through to the most recent Learn One which just Are obligated to pay bundle was designed, there have been four disclosure versions. They certainly were not simple to discover, or even to explore.

You to changed following the homes drama one to unfolded anywhere between 2007 and you may 2010. Actually, the latest government home loan laws itself changed.

This current year, the fresh new Dodd-Frank Wall surface Highway Change and you will Consumer Safeguards Act brought lenders in order to create lending conditions more strict, to slow down the dangers to help you borrowers. By the 2015, brand new CFPB got the first Understand Before you can Are obligated to pay courses. They simplistic the mortgage revelation content the loan providers must promote the individuals.

Mortgage Disclosures Are simple to See, Easy to use-And you will Individualized for Mortgage Buyers.

Now, new CFPB webpages is sold with the Home ownership section. That it a portion of the webpages courses the latest hopeful mortgage debtor thanks to the mortgage-looking to thrill. This has info, suggestions, and you can alerts.

- The borrowed funds Imagine. This indicates the newest arrangement the customer try making – information on the mortgage and all sorts of the appropriate fees. It states the speed, and you can if or not that’s locked from inside the. In case your terms penalize individuals whom spend their month-to-month amount very early, this document claims so. Every informed, the mortgage Estimate might help a loan candidate know exactly what’s on the table, next shop around and contrast readily available mortgage loans over the past days leading up to closure go out! See just what a loan Estimate works out.

- New Closure Revelation. This will help to you end expensive surprises within closure dining table. Does the borrowed funds Estimate match the Closure Revelation? The toolkit shows the person simple tips to examine which file – its numbers and you will mortgage terms and conditions – into same information where they look toward Loan Estimate. This new debtor will get three working days evaluate these models and you will seek advice before-going done with the new closure. See just what a closing Disclosure turns out.

The house Mortgage Toolkit gives borrowers the desired perspective knowing such disclosures. And also the mortgage company provides one for each debtor. See just what the home Mortgage Toolkit (PDF) looks like.

Discover Their Rights, and Understand Law, the CFPB Claims

Think of, all of the financial borrower are entitled to a closing Revelation at the very least three business days before the newest action transfer. This loan places Haleburg may feel like an annoyance to own an upbeat buyer headed to your finishing line. But, too now find, there was a consumer-friendly rationale regarding around three-date several months. Permits customers to evolve their heads on the closing if the something’s a lot less assured. It offers an appartment time whenever a house visitors may get clarifications towards process together with terminology, clarify any questions or dilemma, or maybe even demand alter towards financial arrangement.

At the time, the brand new agency’s on the web publication can be very useful, even for a talented buyer. It gives worksheets, finances versions, and also decide to try role-playing scripts the consumer can use to prepare for real conversations to the mortgage company.

In addition it tells members exactly what home loan con try, and just why to not take action. Saying the most obvious? Yes, however someone would fudge quantity, very maybe they do must be advised it’s going to likely perhaps not avoid well!

Mortgage Companies Have to Approve People in the an unbiased Method. So Need Their Application!

Within the , the newest CFPB provided pointers so you can loan providers with the having fun with formulas, along with fake intelligence (AI). Cutting-line tech helps make all sorts of consumer studies offered to loan providers. These businesses must be in a position to articulate which research variations their choices. They cannot simply state the newest AI achieved it. So the advice alerts loan providers not to merely draw packets on the forms without claiming the specific factors, for the for every case, after they change some body off getting mortgage loans. Whenever they usually do not stick to this information, he could be offensive brand new federal Equal Borrowing Possibility Operate. In reality, brand new Equivalent Credit Chance Operate need lenders so you’re able to identify the specific reasons for refusing in order to thing financing.

What makes it? Because when the lenders tell us straight-upwards as to why our company is deemed ineligible, after that we can understand how to proceed down the road, and you can increase all of our borrowing character correctly. And you can, it reassures all of us one to unlawful prejudice isnt inside gamble. It is ergo the CFPB claims the lender need state the fresh new intricate conclusions you to ran towards assertion. In other words: The things did the newest applicant perform or perhaps not perform?

As well as, brand new CFPB states in its release named CFPB Affairs Some tips on Credit Denials from the Loan providers Having fun with Artificial Intelligence, a loan provider need straightforwardly communicate how come, it doesn’t matter your applicant might possibly be amazed, disappointed, otherwise angered to find out these are generally becoming rated for the studies that can perhaps not intuitively relate genuinely to their money.